[Bitop Review] Global Central Bank Week Kicks Off: Oil Tops $100 – Are Rate Cuts Still on the Table for This Year?

Published on Mar 16th, 2026

This week, global financial markets welcome a critical "Central Bank Super Week," with both the Federal Reserve (Fed) and the Bank of Japan (BOJ) set to announce their latest interest rate decisions. Recent geopolitical tensions in the Middle East, particularly the obstruction of the Strait of Hormuz, have pushed international crude oil prices past the $100 per barrel mark. This violent fluctuation in energy prices brings significant pressure to the global inflation outlook and poses severe challenges to the monetary policy paths of central banks worldwide. This article summarizes the schedule of major central bank meetings this week and explores the potential impact of rising oil prices on macroeconomic data and the stances of decision-making committees.

Geopolitical Conflicts Drive Oil Prices and Inflationary Pressures

The spreading conflict in the Middle East and interference with key energy transport channels like the Strait of Hormuz have placed global energy supply chains at risk. Prices for both Brent Crude and West Texas Intermediate (WTI) have risen significantly. Following the US bombing of military targets on Iran's main export hub, Kharg Island, over the weekend, Brent crude prices surged 3.3%, breaking through $106 per barrel. This bombing may inject fresh turmoil into an energy market already experiencing its greatest volatility in decades. Since the outbreak of the war, soaring oil prices have rippled across various asset classes, triggering inflation fears, pushing up US Treasury yields, boosting the US Dollar, and pressuring global stock markets.

Energy prices are a core component of the Consumer Price Index (CPI), and high-level fluctuations in oil prices will directly translate into "Imported Inflation" pressure. For economies dependent on energy imports, this not only increases operational costs for businesses but may also erode consumer disposable income.

Schedule of Decisions by Major Global Central Banks This Week

This week, inflation risk is likely to be the market's primary focus as eight of the world's top ten central banks announce policy decisions. The Reserve Bank of Australia (RBA) is expected to raise interest rates for the second consecutive month, while other central banks are likely to keep rates unchanged, awaiting clarity on the duration of the conflict.

Reserve Bank of Australia (RBA): March 17

Federal Reserve (Fed): March 17-18

Bank of Canada (BoC): March 18

Bank of Japan (BOJ): March 19

European Central Bank (ECB): March 19

Bank of England (BoE): March 19

Swiss National Bank (SNB): March 19

Riksbank (Sweden): March 19

Fed Maintains Rates: Is a Cut Still Possible This Year?

For the Federal Reserve, inflation concerns triggered by oil prices are altering its monetary policy trajectory. Unlike past periods of quantitative easing, the current decision-making environment is far more sensitive to price changes. Facing an energy shock, internal divisions have emerged within the Fed regarding the risk assessment of a cooling labor market versus a resurgence of inflation. High oil prices may suppress real economic growth, but cutting rates too early risks letting inflation expectations spiral out of control.

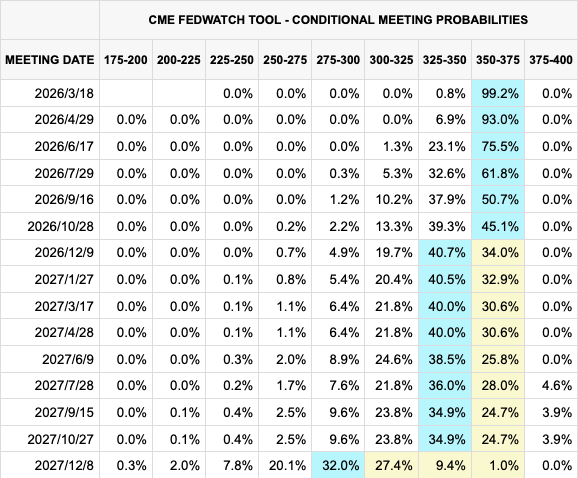

According to CME FedWatch data, due to fears that oil prices will drive up inflation, traders generally believe the Fed will keep interest rates unchanged for the remainder of the year. A rate cut might not occur until December. Prior to the outbreak of the Middle East conflict, the market generally expected room for 2 to 3 rate cuts this year.

Japan Grapples with Oil Prices and Yen Depreciation

The market widely expects the Bank of Japan to keep its benchmark interest rate unchanged on Thursday while assuring the market that it remains on the path toward policy normalization.

Given Japan's heavy reliance on oil imports from the Middle East, Governor Kazuo Ueda is likely to emphasize the necessity of closely monitoring the situation. Persistently high crude oil prices could damage the Japanese economy while exacerbating inflationary pressures. Policymakers must also assess the risk that adopting an overly dovish stance could cause the Yen to depreciate further. The USD/JPY exchange rate has already approached the 160 mark. Japanese Finance Minister Satsuki Katayama stated last Friday (the 13th) regarding the weakening Yen caused by escalating Middle East tensions that, considering the impact on people's livelihoods, the government is committed to "taking all necessary measures at any time and under any circumstances."

Traders will carefully scrutinize the BOJ's statement and Kazuo Ueda's speech for clues, with investors closely monitoring the possibility of a rate hike in April. Sources familiar with the matter stated earlier this month that the possibility of a hike at that time has not been ruled out.

Disclaimer: None of the information contained here constitutes an offer (or solicitation of an offer) to buy or sell any currency, product or financial instrument, to make any investment, or to participate in any particular trading strategy.